Demo Day was a great opportunity to share the CNote story with a diverse group of industry thought leaders.

More than anything, CNote is excited to be recognized as one of “40 of the most ground-breaking early-stage startups” out of a pool of more than 2,000 applicants.Read More

Here at CNote, we fight for financial empowerment. That sounds like a lofty sentiment, but oftentimes it plays out fairly simply in reality: small businesses need loans, and CNote provides community lenders with the funds to make more of these loans. Traveler is one of the many success stories associated with community lending. We’re excited to share the story of Julie Cox and her small business, Traveler.Read More

We are proud to announce that CNote has been chosen out of a pool of more than 2000 companies to present at CB Insights’ Demo Day Conference. We’re honored to be one of the “40 of the most ground-breaking, innovative companies” selected this year. Read More

Cat Berman, CNote’s CEO, was invited to speak at the Women in In Tech symposium at UC Santa Cruz’s Silicon Valley Campus.

The purpose of this event is to: “highlight the experience of women in the tech industry—from established companies to startups and the venture capital firms that support them,” and to “recognize those who have championed the advancement of women in technology through the WITI@UC Athena Awards.” The event also did a great job of assuring that attendees left “with actionable suggestions for overcoming gender-based challenges and improving the workplace climate for all.” Read More

The great folks over at Hint Water were kind enough to host the Challenger Brands conference. A day dedicated to breaking down what it means to be an innovative brand and how that shapes a company, its mission, and its interaction with its customers. Read More

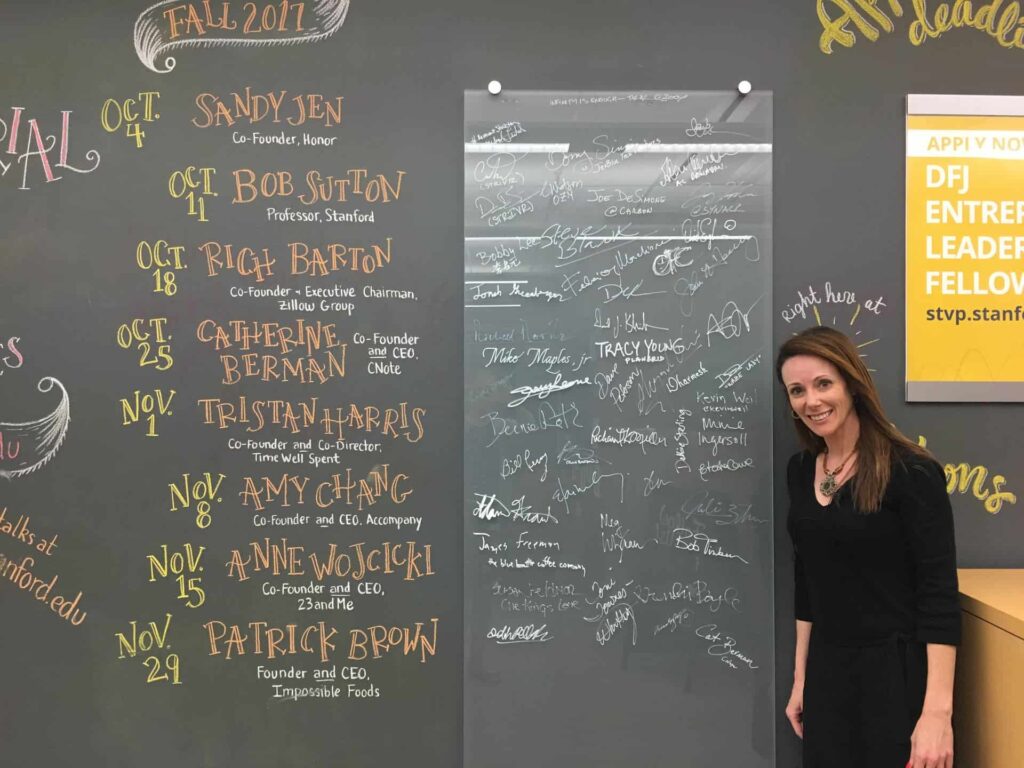

CNote co-founder Cat Berman spoke at Stanford University on October 25th as a part of their Entrepreneurial Thought Leaders Series. Cat’s talk was about Embracing Your Otherness–an inspiring story about events that have shaped her identity and direction as an entrepreneur. It is the journey that ultimately led her to co-create CNote. Read More

At CNote we believe in financial empowerment. That everyone, regardless of their gender, skin color, or birthplace deserves equal economic opportunity. That is why we make financial products for everyone, not just the 1%.Read More

What is a Community Development Financial Institution (CDFI)?

Updated July 2021

Community Development Financial Institutions, more commonly referred to as CDFIs, are private sector, primarily nonprofit, financial institutions that provide loans and other financial resources to Low to Moderate Income (LMI) and BIPOC communities that are often underserved by traditional financial institutions.

CDFIs are federally certified entities. That certification comes from the CDFI Fund, an agency within the U.S. Department of Treasury, which explains that “certification is the U.S. Department of Treaury’s recognition of specialized financial institutions serving low income communities.” The fund has certified more than 1,200 CDFIs and these institutions exist in every state and the District of Columbia, serving rural, urban, and native communities while sharing the primary mission of promoting community development.

CDFIs have roots in the civil rights, anti-poverty, and other progressive movements and can trace their origins to local credit unions and banks that sprang up to address predatory or exclusionary lending practices like redlining in communities across America. They believe in economic justice for all people and are federally regulated to focus their lending and business development efforts in low-income and underserved communities.

This article will explain how CDFIs work, their history, and will contextualize their positive impact on society.

Preamble: The hard work CDFIs have done over the last two decades.

Tanesha Sims-Summers (far right) is the founder of Naughty But Nice Kettlecorn Co. She received a $50,000 loan from TruFund to complete the build-out of a food truck, which allowed her to attend popular events across Alabama to sell her gourmet kettle corn.

Historically, CDFIs are an asset class that is undervalued despite their catalytic impact in communities. The Brookings Institute had the following to say when looking back at decades of historical data on CDFIs:

“CDFIs have succeeded by all obvious measures. A recent sampling of CDFI performance found that 81 CDFIs managing $1.8 billion in assets had provided more than $2.9 billion in financing. They did this with a 1.8 percent cumulative loss rate, consistently low delinquencies, and no losses of investor principle.”

Community Development Financial Institutions (CDFIs), the basics.

CDFIs exist to increase wealth building opportunities for LMI populations and ultimately reduce the wealth gap. They provide loans, financial services and educational resources to those left out of the financial mainstream. CDFIs put a priority on enriching their community over enriching their shareholders and focus on supporting economic growth at the community level, usually by financing small, minority-owned businesses, microenterprises, affordable housing, nonprofit and volunteer organizations, and services essential to revitalizing low-income neighborhoods.

Accordingly, a CDFI’s success is measured not only by their growth and financial performance but also by their impact in underserved communities, including increasing access to capital for minority and female entrepreneurs, new job growth and retention, the creation of affordable housing units and availability of affordable consumer loan products.

Typically, CDFIs come in four different forms, banks, credit unions, development loan funds, and venture capital funds. Each of these four institutional models serves a different part of the community and may have different risk profiles, legal structures, and targeted borrowers.

Ebony Harris, center right, received funding from a CNote partner CDFI. Through her learning center, In Good Hands, she has served families in Jackson, TN throughout the pandemic by providing childcare and support so essential workers in her community could continue to work.

Filling a funding gap.

CDFIs provide financial services and products to individuals and communities that often do not qualify for services by the standards of mainstream financial institutions. These can be individuals that have nontraditional credit profiles and limited assets, younger borrowers with a shorter financial history or previously unbanked groups. CDFIs frequently recognize that living outside the economic mainstream does not make one uncreditworthy. When assessing people and places that have been shut out from mainstream financial tools like FICO scores and home appreciation, CDFIs consider alternative, though no less predictive, underwriting approaches like savings accumulation rates and history of rent and utilities payments.

It should be noted that despite how CDFI underwriting criteria may diverge from a traditional bank’s underwriting criteria, the Opportunity Finance Network (OFN) and Wells Fargo reported in “Innovations in Underwriting” that “innovative underwriting strategies by CDFIs don’t undermine risk management or portfolio quality. Rather, the new strategies analyze past and current portfolio activity to inform new practices.” Without access to affordable flexible capital, these groups’ ability to generate economic growth remains limited. CDFIs, by making their lending activity more inclusive and supportive of their borrowers, are including underserved groups in the financial mainstream.

The loans that CDFIs make have a tangible impact on their local community. Funds are used to support small businesses, develop affordable housing, build community facilities, and launch or expand other community programs.

As noted by Vice President Kamala Harris on June 15th, 2021 when she addressed the nation to announce federal relief funding for small business via a national network of CDFIs, “Community lenders understand the merit in providing access to capital directly to communities, and because they do they add value to those communities, and by extension our entire nation.”

The Community Development Financial Institutions Fund (CDFI Fund), which will be discussed further below, explained the history and the need for CDFIs in more detail:

Community Development Financial Institutions—or CDFIs—emerged in response to a lack of access to responsible and affordable credit and capital in minority and economically distressed communities. The CDFI “movement” took shape in the 1970s with the passage of the Community Reinvestment Act, which encourages financial institutions to meet the needs of all sectors of the communities they serve. Amid growing concerns about the social consequences of investment decisions made by the financial services industry on the nation’s low-income communities, early CDFIs began filling a niche by providing capital and credit in areas that are often difficult for traditional financial institutions to serve. (source)

One example of a successful CDFI with transformative impact is Black Hills Community Loan Fund, a Native CDFI dedicated to creating financial opportunities for economically disadvantaged families who aim to strengthen their financial future in the Black Hills Region of Rapid City South Dakota. With the Native CDFI designation, 51% of an organization’s clientele has to be Native American. BHCLF’s Executive Director estimates that their clientele is coming in at 90% Native American. In Rapid city 10% of the population overall is Native American, and within that population, more than 50% live below the poverty line. BHCLF’s programmatic offerings are centered around financial education, mentorship for entrepreneurs, first-time homeownership, and youth outreach in addition to its lending. You can read more about their impact here.

Executive Director Onna LeBeau (far right) and her full staff for the Black Hills Community Loan Fund

“that financing women and minority homeowners and business owners is not only possible but profitable, and that race and gender are not reliable indicators of financial performance”

“that conventional ideas about managing financial risk have changed and therefore will change in response to evidence that the un-conventional is possible”

“that managing risk in non-financial and non-traditional ways (such as intensive technical assistance) can work”

“that unconventional financial customers are important to conventional financial service companies because they are future customers and solid assets,” and

“that community-centered groups can organize capital, manage it responsibly, pair it with organized people, and create measurable changes in communities.”

The CDFI Fund’s mission “is to expand economic opportunity for underserved people and communities by supporting the growth and capacity of a national network of community development lenders, investors, and financial service providers.” You can read more about the CDFI certification process here. CDFIs, despite being certified by the CDFI Fund, are non-government entities. CNote only invests money with CDFI-Fund certified institutions.

CDFIs, which are certified by the CDFI Fund, then go on to make loans throughout their local communities. The CDFI Fund summarized its model as follows:

“The CDFI Fund supports the mission-driven financial institutions working on a local level that know their communities best. Financial institutions that become certified by the CDFI Fund are eligible to apply for the comprehensive services it offers—including monetary support and training to build organization capacity. The CDFI Fund’s model is competitive and each of its programs provides CDFIs with the flexibility to determine the best use of limited federal resources in their community.”

The aim of the CDFI Fund “is an inclusive economy: an America where all citizens have the chance to participate in the mainstream economy.” CNote supports this goal by driving investor capital to these CDFIs, allowing them to expand their impact and fulfill their mission of financial empowerment.

The economic impact of CDFIs, and the CDFI Fund.

CDFIs have a significant impact on the economic growth of the United States. Nationwide, the CDFI industry manages more than $222 billion, creating jobs, affordable housing, financial health, and opportunity for all. While the focus of CDFIs may be on their local communities, these local activities can have a real impact on the broader economy.

In 2016 CDFIs provided over $3.6 billion dollars in financing to underserved communities (source). While the focus of CDFIs may be on their local communities, these local activities can have a real impact on the broader economy. Here are the 2016 results as provided by the CDFI Fund:

In fiscal year 2016 alone, CDFI Program awardees reported that they provided $3.6 billion in financing to homeowners, businesses, and commercial and residential real estate developments. These developments include the construction of community facilities in communities that might not otherwise have these amenities. In addition, CDFI Program awardees financed over 13,300 businesses and provided more than 427,000 individuals with financial literacy or other training. Similarly, in 2016, over $3 billion in loans and investments were made possible under the New Markets Tax Credit Program, with over 74 percent of the loans and investments made in Severely Distressed Communities. This critical financing contributed to more than 10,000 jobs and an estimated 26,000 construction-related jobs; and resulted in more than 600 affordable housing units, 10.1 million square feet of commercial real estate, and 5,500 businesses receiving financial counseling or other services.

According to the Opportunity Finance Network (OFN), a network of CDFIs, through its fiscal year 2018, its member CDFIs provided more than $75 billion in lending. This led to the creation or maintenance of 1.56 million jobs, the start or expansion of 419,150 businesses and microenterprises, and the development or rehabilitation of over 2.1 million housing units and 11,592 community facility projects.

This data shows just how concrete of an impact community-focused lending can have on the broader economy. These investments in small businesses and community development lead to job growth and economic prosperity. In summary, CDFIs help deliver economic opportunity to everyone

To that point, this video illustrates the kind of opportunity CDFIs provide to borrowers:

In addition to capital, CDFI’s differentiate their success and impact via technical assistance. They provide tailored support and guidance to the entrepreneurs they support. These CDFIs know the common issues small businesses in their communities face, and they can help them overcome obstacles to grow and become sustainable entities that create jobs and increase the tax base.

An example of this local expertise and guidance was the ongoing support that Access to Capital for Entrepreneurs, ACE, was able to provide to budding franchisee Felicia Parks. Felicia, a veteran, decided to open a Jimmy John’s store in Atlanta with her sons but being a first time business owner, she needed some help. Initially, ACE was able to assist Felicia with her business operations via a business coach; however, when COVID-19 hit, Felicia received a bridge loan from ACE to cover operating costs until she could secure a PPP loan through another lender. Unlike many of the business owners around her, Felicia’s Jimmy John’s never had to close its doors. Now, as she’s preparing for life after the pandemic, ACE has provided guidance and advice to help Felicia navigate the next 12 months, and Felicia is making use of ACE’s online resources on marketing, management, and finance, all geared toward getting her business back up and running after COVID.

Felicia Parks (far right) is the owner of a Jimmy Johns location in Atlanta. When COVID-19 hit the area, her sales dropped 64%. She connected with a CNote CDFI partner, who provided a bridge loan that enabled Felicia to keep her head above water and her store open.

CDFIs do much more than cut a check and walk away. They provide guidance, support, and expertise. They share success with their borrowers. By extension, every investor at CNote shares in the success of our partner CDFIs as they work to increase access to capital for communities in need and create more inspiring stories like that of veteran turned entrepreneur, Felicia Parks.

Are CDFIs riskier because they invest in underserved communities?

The risk profile of CDFIs has been assessed and the reality is that CDFIs do not present significantly more risk than non-CDFI financial institutions.

CDFIs also have the benefit of certain federal programs like the CDFI Bond Guarantee Program, which provides federal guarantees for bonds issued by CDFIs that make investments for eligible community or economic development purposes. We note that every investors’ appetite for risk can vary. While the research cited below can help guide an investment decision, it is not investment advice; Always consult with a financial adviser to find the investment option that is best for you.

In late 2014, two independent reports on the CDFI program “found that CDFIs have no more risk than conventional lenders and that they perform nearly just as well as mainstream financial institutions.” The first report, CDFIs Stepping Into the Breach: An Impact Evaluation Summary Report, undertaken by Michael Swack, Eric Hangen and Jack Northrup from the Carsey School of Public Policy at the University of New Hampshire made the following key conclusions:

CDFI loan fund lending fills market gaps for key underserved low-income populations;

CDFI loan funds deliver between roughly two-thirds to over ninety percent of all loan volume to borrowers living in a CDFI Fund-designated Investment Area;

From 2005 through 2012, CRA reported lending decreased while CDFI loan fund reported lending more than tripled, and during the recession, this activity provided a counter-cyclical boost to the economy;

CDFI loan funds provide borrowers that may not qualify for loans from mainstream sources with loan terms and interest rates that are still comparable to mainstream products; and

The CDFI Fund is the second largest-source of equity to CDFI loan funds after internally-generated funds.

CDFI banks and credit unions were found to have no more risk of financial failure than mainstream financial institutions, even after controlling for the CDFIs’ degree of involvement in the mortgage market during the financial crisis; and

Despite serving predominately low-income markets, CDFI banks and credit unions had virtually the same level of performance as mainstream financial institutions.

This research suggests that CDFIs, when managed properly, can deliver returns at or below the risk profile of their non-CDFI counterparts.

CDFIs as Economic First Responders

CDFIs have consistently operated on the front lines of economic disasters such as 9/11, Hurricane Katrina, Superstorm Sandy, Hurricane Harvey, and the 2008 financial crisis, providing economic relief to American communities when they need it most. The Federal Reserve has recognized CDFIs as “economic shock absorbers” that continue to effectively serve their communities even amidst the most catastrophic economic conditions. Not surprisingly, we’re seeing that now in full force with this pandemic and the associated economic fallout.

The COVID-19 health crisis has had a traumatic and far-reaching impact on American communities, especially low-income communities and communities of color where small businesses play an essential role in sustaining economic growth. CDFIs have been essential to recovery as a crucial lifeline for small businesses across the country during the pandemic, and even for decades before.

During the Great Recession, when mainstream finance retracted lending, CDFIs maintained their lending activities and kept capital flowing to low income communities. With consistently low loan loss rates—a cumulative 0.73% from 1999-2017 that outperformed the 0.92% loan loss rate of FDIC-insured institutions in that same time period— CDFI lending has proven effective and successful in changing economic conditions.

Brighter Beginnings (staff pictured above) is a non-profit which provides vital medical and social services to low-income and minority families in Richmond and Oakland, California. They received a critical PPP loan from CNote partner, Self-Help Federal Credit Union, which allowed them to rehire employees, and continue serving the community.

After the pandemic began, a subset of about 300 CDFIs delivered $7.4 billion in PPP loans within the first three months. For comparison, JPMorgan Chase, which is the largest PPP lender and whose assets total $2 trillion, made only four times as many PPP loans as CDFIs did while being about nine times the size of the CDFI industry. In 2021 when the PPP portal reopened for an additional round of federal relief capital at the beginning of 2021, CDFIs were granted an exclusive access period to fulfill loan applications in recognition of their unique position to reach those being hit the hardest by the health and economic effects of the pandemic.

CDFIs have led the way for decades in supporting recovery efforts and it has been no different during the pandemic, and are essential to the health of our economy as a whole.

Investing in CDFIs as a way to support economic inclusion, economic justice and to reduce the wealth gap

The webinar introduces Community Development Financial Institutions (CDFIs) as an impactful and competitive investment. Highlighting their strong history of providing economic resources to financially underserved communities across America, helping to create jobs, fund small businesses, and support affordable housing development.

Large banks and foundations of all sizes have been investing in CDFIs for decades. Until recently, investing in a diverse pool of CDFIs at scale presented significant challenges for all but the savviest of investors. Now, with CNote, investors of all sizes can deploy capital across a diverse pool of CDFIs with ease.

This presentation provides an overview of the CDFI industry, its history, how CDFIs are certified by the Department of Treasury, their mission and the types of investments CDFIs make in the communities they serve. Most importantly, this webinar explores the way increased capital access and CDFI lending activities can have a transformative effect.

“Even if you never apply for a loan from a CDFI, you should care about them. These institutions serve in places that the financial sector historically hasn’t served well. And that lifts our whole economy up.”

Secretary Janet Yellen

How do I invest in CDFIs?

Prior to CNote, investing in a CDFI was a difficult, rigorous, and generally limiting process. CDFI investments can often be bespoke undertakings.

Today, anyone can invest as little as $1.00 in CDFIs to earn a higher return on their savings and have an impact on communities across the country. CNote optimizes for impact within its portfolio of CDFIs, and is the first company to make CDFIs, as an asset class, available to all investors.

The Kind of Company, and Entrepreneur, That Inspires Us

At CNote, we a believe in underdogs. Our mission is to deliver financial empowerment, both to savers, and to financially underserved communities. Your investment in CNote drives community development projects, and provides the funding female and minority entrepreneurs rely on to get their businesses off the ground.

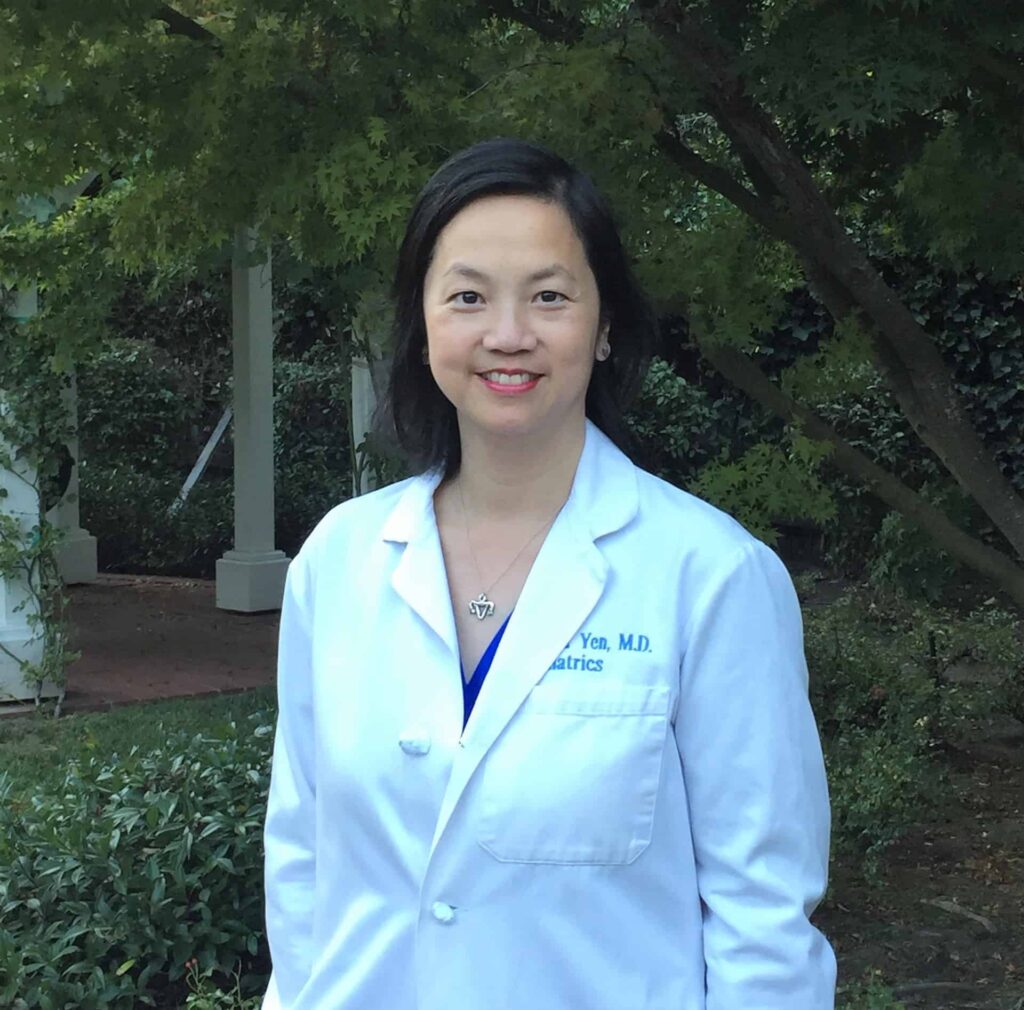

Often, its hard to envision what these companies might look like, who runs them, and how they impact the world. Today, we highlight Pandia Health and its CEO, Sophia Yen, MD, MPH, as an example of the kind of change that can occur when a motivated entrepreneur is given the capital to execute on her dream.

Dr. Sophia Yen has over 20 years of experience in medicine. She serves as a clinical Associate Professor of Pediatrics in the Division of Adolescent Medicine at Stanford Medical School. She graduated from MIT, UCSF Medical School, and UC Berkeley with a MPH in Maternal Child Health. Dr. Yen co-founded Pandia Health and enjoys educating the public and other physicians about birth control, acne, weight management, and other adolescent health issues.

The Pandia Health Peace-of-Mind, Taking The Pain Out of Reproductive Health

For the vast majority of the women who use it, birth control can be a real pain in the uterus. It’s a pain to swallow a pill every day. It’s a pain to drive to the pharmacy once a month to refill the prescription. But most of all, it’s painful to stress over the possibility of an unplanned pregnancy and the life-altering impact it can have.

Dr. Sophia Yen, co-founder and CEO of Pandia Health, calls it “pill anxiety.”

“You’re going through your pills and you get to that last week; and if you don’t get to the pharmacy, there will be a dire consequence. And so you have that stress in the back of your mind every single month,” she explains, speaking of her own experience as well as that of millions of other women. “And so that is the goal of Pandia Health…to cure women of this pill anxiety.”

“Set it and forget it; don’t run out on our watch.”

Indeed, when it comes to birth control, Pandia Health has taken over the watch. Through its website the company offers two main services: 1) monthly deliveries of birth control to the customer’s door, billed to insurance; and 2) telemedicine prescriptions costing a flat rate of $39, valid for a year. By taking over the responsibility of refilling birth control, Pandia Health has cured pill anxiety with what Dr. Yen dubs “Pandia peace-of-mind.”

Pandia Health’s Mission, and Drive, Comes From its Founder

From the way Dr. Yen speaks of her company, it’s clear that it is a source of pride and joy to her: “We are busting open access, and that’s what makes me happy: saving women stress, preventing unplanned pregnancy.”

An MD and MPH in Maternal Child Health, Dr. Yen has a demonstrated passion for women’s health and reproductive rights. Pandia Health is a natural extension of that focus. Indeed, it was in preparing for a talk about birth control that she conceived the idea of Pandia Health.

“I came across this statistic that one of the top three reasons women don’t take their birth control is they don’t have it on hand,” she recalls. “And I said, ‘This is easily solvable.'”

But her passion to solve such problems began even before that.

When Sophia Yen was 15, she ran a pregnancy test. The test wasn’t for her, but for her 13-year-old client in a pregnancy counseling program. And it came back positive.

“That was life altering for that patient forever,” Dr. Yen recounts. “It just made me sad to see the two different trajectories: I was going to head off to college and off to medical school, and she was going to head off to a life of teen pregnancy. And so I realized then how critical it is that people have access to birth control and comprehensive sex ed.”

Since then, she has not stopped “busting open” that access. Nowadays she continues to take joy in her work, motivated by the impact she can have on young lives with her work.

The joy is clear in the way she treasures her customers. Admiring their initiative to prevent unplanned pregnancy and make their lives easier, she calls them all “beautiful” and includes “fun things, randomly” in their shipments, such as chocolates, sunglasses, and condoms. On the rare occasion that there’s a problem with a refill date, she contacts the patient’s pharmacy to make sure patients have access to a new prescription before the pills run out.

In the end, the personal and professional commitment that characterizes Dr. Yen’s work comes from a passion to empower women to control their own destiny. She’s said that her life’s work is to make women’s lives easier by saving all the unnecessary effort that goes into getting and using birth control. Her commitment to reproductive health is consistent, from the bumper sticker on her car, to the playful uterus-shaped pendant that adorns her necklace.

Turning Challenges Into Opportunities

In the early stages Pandia Health’s founding, the passion was there, but the money was not.

“The financial part is always ugly in the beginning…Funding-wise, you just have to bootstrap it or suck it up until you get money,” says Dr. Yen.

But her efforts to “bootstrap it” and secure funding at investment pitches were met with some resistance: namely, the barrier of many potential investors not understanding the problem because they had never experienced it personally.

In addition to uncertainty in the cause, there was also some uncertainty in Dr. Yen herself as a potentially successful entrepreneur. From the female founders before her Dr. Yen quickly learned to “never bring your male CTO or co-founder next to you, because they [investors] will be looking to him to approve, even though you’re CEO, even though it’s your idea, even though you brought the whole team together.”

Aside from gender bias, there was the perceived disadvantage of her being a physician (who are not traditionally credited with good financial intuition) and being a mother (who are not traditionally credited with having much time on their hands).

But rather than being weaknesses, Dr. Yen argues these unique life experiences helped her succeed. As a physician and mother, she was accustomed to working hard. And as a woman entrepreneur, she was able to anticipate being judged on accomplishments rather than potential. She knew she had to work harder and be more proactive than most if she wanted Pandia Health to succeed. So, she arranged a team of five multi-disciplined founders to make sure that they “could absolutely do it” before they asked for money.

Talk about weaknesses being turned into strengths.

It turned out that the “weaknesses” perceived by some investors became Pandia Health’s saving grace in other circles of investors. Namely, the cause for accessible birth control that turned 70-year-old male investors away, was admired and supported by organizations who liked to invest in social entrepreneurship, like OneWorld and Women’s Startup Lab.

Through such organizations, Dr. Yen was able to not only secure investments, but also access networks where she could exchange resources with other “femtech” companies for the mutual benefit of both.

Pandia Health’s Impact

Now, three years after her initial idea, Dr. Yen continues to strive for solutions to the women’s health issues she is passionate about. With an adaptable mindset picked up from MIT, and a work ethic refined in medical school, she pivots her business in directions best suited to her customer’s needs: starting an ambassador program to increase awareness on college campuses; raising money to expand services nationwide and establish Pandia Health’s own pharmacy.

Of her company’s growth, she says, “We see a future where we start with birth control, we gain women’s trust, and we grow with them as they grow. So there’s huge potential, and you have to be flexible, you can’t be in a set mindset.”

But although the growth path is open to change, one thing is constant: The company will adapt itself to respond to women’s needs. It has done so from the very beginning and will continue to do so. And that is what women can count on for continued Pandia Health peace-of-mind.

Dr. Yen has shown us the impact a dedicated entrepreneur can have on the world. The money invested in Pandia Health has been a force for good in the lives of the women the company has served. Because Pandia Health predates CNote, we have not deployed any investment dollars in Pandia Health directly, but we will continue to work to drive dollars to entrepreneurs like Dr. Yen and share their inspiring stories, regardless of their funding source.

Pandia Health Today

Pandia Health is looking to expand its services nationwide and continue serving women in the most convenient, pill-anxiety free way possible. Their work is more relevant than ever, now that affordable birth control has become even less of a guarantee given the recent defunding of insurance-covered contraceptives.

For FAQs with Dr. Yen about birth control, women’s health, and more, take a look at their Youtube channel and blog.

Dr. Yen encourages those interested in women’s health and advocacy to support the Silver Ribbon Campaign. That charity serves as an advocate for the respect of women’s reproductive rights.

Additionally, Pandia Health has created a Birth Control Fund to provide “financial assistance to women in need of access to birth control.” You can read more about that program here.

CNote made history with its launch to non-accredited investors on September 27, 2017. We are the first company to offer everyday investors seamless access to the reliable return and social impact of CDFIs. This launch was built on thousands of hours of effort. We are grateful for all the support and help we’ve had along the way.

Launching the first impact-focused savings product is a huge step towards our goal of delivering financial empowerment to even more people.

At CNote, we know trusting someone else with your money is a huge deal, that is why we built multiple layers of protection into every CNote account. These layers of redundancy help minimize the risk of capital loss. While our CDFI partners have never lost a single investor dollar, we want you to feel confident about your investment in CNote. Knowing that your investment has a strong history of consistent performance is one thing, knowing that you’re likely protected even if something goes wrong is even better.

The infographic below helps explain CNote’s Triple Protection Plan. If you want to read further, you should review our Risk & Return page.

We’re excited to announce that CNote has been selected as one of the top 100 companies to compete for TechCo’s startup of year!

WooHoo! Put your party hats on.

This means we’ll be pitching at the Innovate and Celebrate conference in San Francisco. We’re hoping a little home-field advantage works in our favor. This is the first time CNote has presented at this event so it promises to be exciting.

We’re looking forward to sharing CNote’s story with even more people, and seeing what some of the brightest and most innovative entrepreneurs are up to. Along with spreading the word about our mission of financial empowerment, we’d be lying if we said we we’rent just a little fired up for some friendly competition. Also, its hard not to discount all the inspiration you come away with after attending an event like this.

Click the very official badge below to see the other semifinalists and cast your vote for CNote!

We’re also excited to announce that of the 100 semi-finalists, 29 have female founders or co-founders. As you likely know, CNote is helmed by our female co-founders, Cat and Yuliya. CNote, is in good company on this list and we’re excited to see more female entrepreneurs get the recognition they deserve. Hopefully, it will be 50/50 in the near future!

After months of working with the Securities and Exchange Commission (SEC) and our dedicated legal team, we are delighted to announce that we have been qualified by the SEC to offer our product to everyone! You can review our offering circular to learn more about CNote, and the innovative financial product we have brought to market.

For current account holders, nothing will change. We’re grateful you’ve been with us from the beginning, and you’ll still receive the same great return with a positive social impact.

For the list of non-accredited investors waiting to earn 2.5%, we are excited to welcome you with open arms! You should expect an email shortly explaining how you can transfer funds and start earning money. We know some of you have been waiting for quite a while, we are excited to welcome you to the CNote family.

CNote Launches to Turn Americans’ Savings into Democratized Impact Investments

By parking your extra cash with this fintech startup you can earn 40X more money while driving economic opportunity across the United States.

September 27, 2017 // Oakland, CA // CNote, which offers up to 40x the return of a typical savings account, is announcing the public launch of its impact-focused financial platform. Previously in a testing a period with accredited investors, who collectively committed more than $9 million in savings, the Oakland-based startup is now open to everyday savers and non-accredited investors with no minimum deposit required. The startup’s flagship product has made history as the first high-yield impact product to be qualified by the Securities Exchange Commission (SEC) for mass market.

Functioning as a high-yield savings product, CNote pools deposits from multiple savers and invests it in highly-impactful, but largely unknown, Community Development Financial Institutions (CDFI). CDFIs are U.S. Treasury certified, and exist to help finance and support underserved populations like women and minority business owners.

CNote provides a 2.5% return to savers, a stark contrast to the 0.1% – or less – that most savers receive from traditional banks.

Founders Catherine Berman and Yuliya Tarasava built CNote out of a desire to help savers do good and do well. The result of their collaboration is the first savings product to deliver outsized returns and positive social impact.

In December, the team ran a successful test with accredited investors, with over $9 million in committed savings under Reg D. In March, the company was selected as Best Startup Pitch Company at SXSW, as well as the Fintech Category Winner.

As the first platform of its kind, CNote is launching to the general public today with a cohort of CDFI partners, including CDC Small Business and Pursuit Lending. They each provide a range of services and financing options for business owners who are often ignored or underserved by traditional financial institutions.

“There’s an estimated $300B of cash that just sits on the sidelines collecting dust in our savings accounts. There’s no reason we can’t unlock it for good by putting that money to work in our communities, while driving better returns for you,” Catherine Berman, CEO and Co-Founder of CNote said. “We could not be more thrilled to open our platform to everyday consumers and smart savers, and we hope people will see this as an opportunity to think outside the bank.”

This product is the first of CNote’s suite of competitive-yield, high-impact products that seek to redesign finance with a focus on financial inclusion and empowerment.

Interested CNote users can learn more about the platform at www.mycnote.com.

###

About CNote

Founded in 2016 by Catherine Berman and Yuliya Tarasava, CNote is a financial platform for socially-conscious savers and investors. The company’s flagship product offers a 2.5% return on savings — and 100% social impact — by tapping into Community Development Financial Institutions (CDFIs), which exist to help finance underserved small business owners. In September 2017, CNote became the first competitive-yield financial product to be federally recognized and available to the mass market with no minimum and no fees.

In March 2017, CNote was selected as Fintech Category Winner at South by Southwest. The venture-backed fintech company currently operates with a team of 8 out of Oakland, California.

CNote Launches to Turn Americans’ Savings into Democratized Impact Investments

By parking your extra cash with this fintech startup you can earn 40X more money while driving economic opportunity across the United States.

September 27, 2017 // Oakland, CA // CNote, which offers up to 40x the return of a typical savings account, is announcing the public launch of its impact-focused financial platform. Previously in a testing a period with accredited investors, who collectively committed more than $9 million in savings, the Oakland-based startup is now open to everyday savers and non-accredited investors with no minimum deposit required. The startup’s flagship product has made history as the first high-yield impact product to be qualified by the Securities Exchange Commission (SEC) for mass market.

Functioning as a high-yield savings product, CNote pools deposits from multiple savers and invests it in highly-impactful, but largely unknown, Community Development Financial Institutions (CDFI). CDFIs are U.S. Treasury certified, and exist to help finance and support underserved populations like women and minority business owners.

CNote provides a 2.5% return to savers, a stark contrast to the 0.1% – or less – that most savers receive from traditional banks.

Founders Catherine Berman and Yuliya Tarasava built CNote out of a desire to help savers do good and do well. The result of their collaboration is the first savings product to deliver outsized returns and positive social impact.

In December, the team ran a successful test with accredited investors, with over $9 million in committed savings under Reg D. In March, the company was selected as Best Startup Pitch Company at SXSW, as well as the Fintech Category Winner.

As the first platform of its kind, CNote is launching to the general public today with a cohort of CDFI partners, including CDC Small Business and Pursuit Lending. They each provide a range of services and financing options for business owners who are often ignored or underserved by traditional financial institutions.

“There’s an estimated $300B of cash that just sits on the sidelines collecting dust in our savings accounts. There’s no reason we can’t unlock it for good by putting that money to work in our communities, while driving better returns for you,” Catherine Berman, CEO and Co-Founder of CNote said. “We could not be more thrilled to open our platform to everyday consumers and smart savers, and we hope people will see this as an opportunity to think outside the bank.”

This product is the first of CNote’s suite of competitive-yield, high-impact products that seek to redesign finance with a focus on financial inclusion and empowerment.

Interested CNote users can learn more about the platform at www.mycnote.com.

###

About CNote

Founded in 2016 by Catherine Berman and Yuliya Tarasava, CNote is a financial platform for socially-conscious savers and investors. The company’s flagship product offers a 2.5% return on savings — and 100% social impact — by tapping into Community Development Financial Institutions (CDFIs), which exist to help finance underserved small business owners. In September 2017, CNote became the first competitive-yield financial product to be federally recognized and available to the mass market with no minimum and no fees.

In March 2017, CNote was selected as Fintech Category Winner at South by Southwest. The venture-backed fintech company currently operates with a team of 8 out of Oakland, California.

Note that effective January 1, 2019, the rate on all CNote accounts has increased to 2.75%.

If you are new to CNote you may have some questions. How do you pay 2.5%? How safe is CNote? Where does my money go?

The video below should help answer most of these questions in only 60 seconds.

If you still want to learn more, you may want to visit our FAQ or our Risk & Return Page.

Transcript of the video:

So you may be wondering, how does CNote earn you 2.5% on your savings when your bank pays you next to nothing?

Unlike banks, CNote doesn’t use your savings to fund credit cards or mortgages. We lend your deposits out to US-Treasury-certified community lenders that have more than 20 years of proven financial performance.

These community lenders build our schools, fund our community centers and invest in the women and minority-led businesses that keep our communities thriving.

Until now, access to these high performing community lenders was only readily available to large banks and foundations. CNote’s proprietary technology gives every-day investors like you access to these investments.

Also, unlike banks, we return the profit earned on these loans back to you instead of keeping it to pay big bonuses and excessive overhead. We never charge you any fees, and the 2.5% goes straight into your pocket.

Welcome to a world of finance driven by good, not greed.

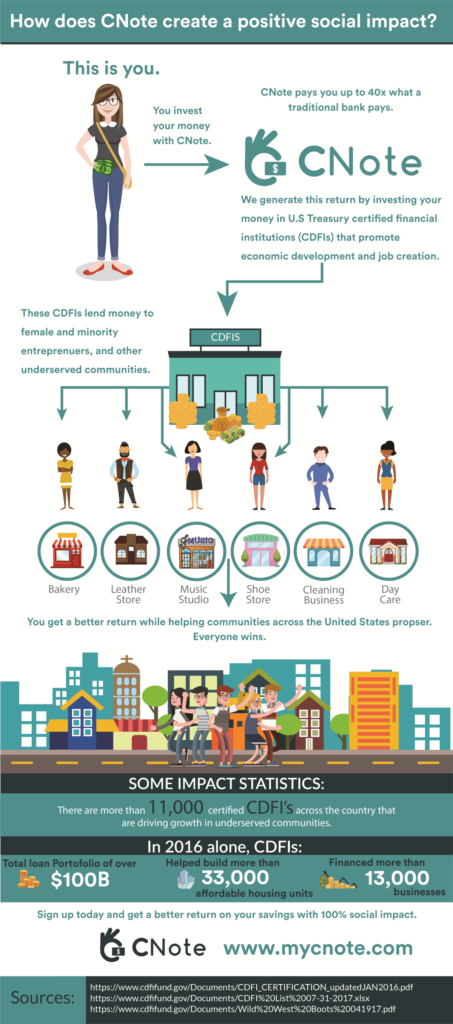

A lot of potential customers want to understand how CNote generates great returns along with helping financially-underserved communities across the United States. This simple infographic helps explain CNote’s model for generating a positive social impact.

Note that effective January 1, 2019, the rate on all CNote accounts has increased to 2.75%.

This video explains how CNote is able to deliver a higher return on your savings while driving prosperity in communities across the United States. It highlights the institutions we invest in, their proven financial track record, and the tangible impact that they have.

Finance shouldn’t be complex or hard to understand. This video should help answer some of the questions you may have about CNote.

Earn more. Do good. Feel great.

If you still want to learn more, you may want to visit our FAQ or our Risk & Return Page.

Odds are that you have heard of the guy pictured below. He’s fundamentally changed the way we look at the physical world. Yet, despite his amazing contribution to science, he had some pretty significant thoughts about other important areas of life as well. Read More

In the startup world, six months can feel like a lifetime.

Indeed, its been about six months since CNote won the Fintech Category and took home Best Startup Pitch Company at SXSW. A lot has changed, our team has grown, but the most important things have stayed the same.

Same mission, prettier website

Despite growing as a company since March, our focus and core goals of offering a better return with tangible social impact have not changed.

In the future, the fashion might change, and the video cameras might get better, but we believe this pitch, delivered by co-founder Cat Berman, will reflect our core principles for years to come. That is why we decided to share it again as a reminder to our community, employees, and customers about the goal we are working towards. We are working to make finance more inclusive; where great returns are not reserved for the wealthy few. We are also crazy enough to think that you can get a great return while bringing prosperity to financially underserved communities and individuals across the country.

The pitch

Hi, my name is Cat Berman, co-founder of CNote. Before I started CNote I was Managing Director at Charles Schwab and there I stumbled on this shocking finding, American’s are sitting on 300 billion dollars in just in case cash, not emergency fund cash but literally just in case cash. These are dollars sitting in our checking and savings accounts making nearly zero percent. What’s worse, we’re actually losing money, you see savings accounts don’t keep up with the rate of inflation anymore so you and I are losing about one percent of our nest egg, simply by leaving it in the bank, until now.

CNote delivers a return on your savings, two and a half percent, that’s 40 times better than traditional banks with 100% impact. We do it by working with a little known, but highly successful, financial tool called CDFIs. CDFIs aren’t new, they’ve been around for 20 years, they’re certified by the treasury department and nearly every major US bank uses CDFIs. What’s more, is every dollar invested in CDFIs goes to under-severed communities like women and minorities. CNote is the first and only company to unlock CDFI return and impact for every day savers.

How’d we do it, by creating a proprietary technology to optimize our savings across CDFIs. The team includes my co-founder Yuliya Tarasava, she ran a 10 billion dollar risk management function, Nikhil Desai our VP of Engineering was Senior Developer at Lending Club and this will be my 3rd start up. My last start up, Global Brigades is now in 5 countries. Last summer we launched our beta and to date we have over 7 million in savings on our platform. We’re excited for this year where we’ll be rolling out to potential 8 million customers with our 1st channel of distribution partner and donor advised fund. The average CNote saver starts by making 10 dollars a year on their savings account and with CNote ends up making over 500 dollars a year, just by signing up in 3 minutes.

You work hard for your savings, it’s time your savings will work hard for you.

Earn more with good karma. Welcome to CNote.

Click below to watch.

We’ve got a lot of new and exciting things on the horizon. We look forward to sharing more of our story with you here.

Join us, as we work to make finance more inclusive.

Mamacitas Cafe, a specialty coffee and baked goods retailer in Oakland, is different. A lot of other coffee shops may say the same. Be it their brewing methods, the coarseness of their grind, or the music heard playing in the background, this cafe is on a mission to elevate women of color. This coffee shop offers it’s employees professional training, community building, and the ability to directly take part in day-to-day business tinkering and planning.

Impact First. Profit Second.

As with any coffee shop, Mamacitas Cafe was not immune to the challenges of a newly formed business. From payroll, equipment purchases, and construction to the unexpected removal from a commercial space it took serious commitment and foresight to stick to their guns and forge their own path. According to founder Shana Lancaster, at one point cash flow was barely enough to cover the rent for a temporary space let alone afford milk for the next day of business! Regardless, the founder’s resolve remained strong as taking on debt was not going to be an option.

Why? Well, to start, they knew they wouldn’t qualify. But most importantly, traditional sources of capital would have put too much pressure to focus on what did not matter, such growing way too fast. So, Mamacitas Cafe went the alternative route and successfully completed two Kickstarter Campaigns and took out a Kiva Zip loan.

The co-founders are equally invested in their Oakland community as they are in their business. Growing up in the city and having participated in a variety of women and other minority groups, they have a clear point of view on the community issues. Young women of color are clearly a forgotten pool of talented, creative, and driven people who are continuously challenged to prove themselves time and time again. And the Mamacitas’ focus on empowerment, love and growth is what has put them on the map. All the while tripling their revenue in just two years!

Success by Partnerships

Mamacitas Cafe, although awaiting their first commercial kitchen space, has been successful for the past two years due to their strong relationships in a values aligned community. From a subsidized shared kitchen space in exchange for food retail training to women of color to pop-ups around the East Bay this business will always do good for its community.

Small Business is Good Business

In the end, we should be remembering what it is a company does outside of its’ concrete walls. Mamacitas Cafe can do that in so many words that it is hard to choose the right ones. Growth. Empowerment. Resiliency. Earned Income potential. Education.

It doesn’t matter though. Because no matter what you or I think of them, they will always put their Sisters first. With quirky, heavenly donuts on the side.

For San Franciscans, coffee drinking has become a ritual and an experience to be savored. And discovering coffee shops offering new flavors, aromas, and brewing methods has become a popular pastime in the city. In 2015, Belen and her husband decided to offer a completely unique coffee drinking experience to the San Francisco coffee-loving community. Combining their passions for baking and coffee, they opened Zo11 Coffee Roasters on Fillmore St. While starting the business meant a major step into the unknown, Belen believed that because they were doing what they loved they would be able them to face and overcome any challenge together. And they did exactly that.

A founder driven by passion

“Follow your passion” became Belen’s compass to navigate. And for Belen this meant working tirelessly and taking deliberate steps towards attaining her goal. Upon arriving from Ethiopia in 2001, Belen embraced her love for style and clothes and enrolled in a San Francisco-based program to become a fashion designer. After her first son was born, she exited the fashion profession to spend more time with her family. But her new job at the dental office was not satisfying to say the least. This is when her husband Alex started conversations about opening a cafe.

Local business offers an authentic experience flavor

For Ethiopians, coffee is not just a drink that wakes you up in the morning to prepare you for work. Coffee is ingrained in their identity and culture. The couple envisioned a space where they could replicate the atmosphere and the magic of the coffee ritual as it is experienced in Ethiopia. Alex has been supplying authentic Ethiopian coffee to local farmers markets for years, so finding high quality beans was not a problem. Belen, who had basically lived in her mom’s kitchen since she was a child grew up baking and experimenting with recipes. Banana bread became her specialty.

Alex and Belen had the skills and experience to pursue their passion, but getting the actual real estate seemed impossible at times. Having lived in the Fillmore neighborhood for a few years, Belen knew exactly where she wanted to have her cafe. However, the spot was owned by the local Ethiopian church and renting it out was not an easy task. It took two years of negotiations, lots of patience, and many repairs before they could even step foot into the space.

Difficult decisions for a local business

When it came to funding their business, Belen and Alex decided not to take any outside money because they were scared of being taken advantage of by a complex financial system. Instead, they maxed out their credit cards and put their life’s savings into the business. It was a risk they were willing to take, which ultimately enabled them to open their cafe. Belen was waking up every morning at 4 am to make pastries with freshly sourced ingredients from local farmers markets, getting inspiration from Youtube and Pinterest, and modifying recipes to make them healthier with her unique twist.

Lessons of a small business owner

Now, almost two years later, Belen says that despite the hardships she would not change a thing. Through her experiences she has noticed that life is all about learning. You can’t change the past so you’d better treat it as a lesson, brush off negative feelings and carry on. Today, Belen and Alex continue to dream big and are planning to expand with a second floor of seating and to redesign the whole cafe area.

A business that fosters community (and delicious donuts)

With a confident smile, Belen proudly shares that the coffee shop for her and Alex is not just a business – it is a community they built through their determination and compassion. They genuinely care about their customers and cherish each conversation and interaction. And Z011 customers especially love Belen’s authentic donuts made every Sunday. Hope you can try them soon too!

Running a small business is a huge challenge. Even with the best-laid business plan and capital to spare, if you want to follow the long road to success you are going to need some help. Be it financial planning or access to skilled employees, a small business’ ability to leverage this help is critical to surviving and growing. We spent time with Prospect Cleaning Service to learn more about their experience working with Pursuit, one of CNote’s CDFI partners. Read More

MAFIA Bags is more than just a series of stylish, functional, and sturdy bags, totes, backpacks and accessories. It is a company which represents community and cohesiveness around two inspirational goals. To give new life to materials and to transform the way we do business.

Started in 2012 by brother and sister Marcos and Paz Mafia, MAFIA Bags began with an idea to upcycle used sails into backpacks. Their idea originated from the need for a durable backpack to carry their wetsuits while traveling to surfing locations around the world. And since day one, as they have perfected the design, MAFIA Bags has also fostered the tradition of community by bringing on friends and employing locally to scale the business. Even as the business has expanded from their hometown in Buenos Aires to a small rented garage in Outer Sunset and multiple locations around the world, MAFIA Bags has remained dedicated to maintaining its core values of sustainable design with minimal impact.

If you spend thirty minutes at their store in SoMa you will see this immediately. Your jaw will drop at the colorful variety of bags and totes hanging on the walls, which will make you doubt that these are made of upcycled materials. You will likely spend too much time exploring exhibits of past design collaborations with major brands like Airbnb, or you’ll marvel at the boxes of sails from around the world ready for assembly by any of their talented designers. It will be hard not to feel inspired.

For a small business based out of the bustling SoMa district in San Francisco, California, to continue their journey as a challenger brand may feel like a tall order. Yet, it is difficult to say that MAFIA has not lived up to the hype just yet.

Beginning with a successful Kickstarter campaign, MAFIA Bags has collaborated with many global brands. These include Patagonia, Sperry’s, Vans, the Stanford Design School and more local groups like SustainableSurf.org. On your next trip to Buenos Aires, Barcelona, Shibuya (Japan), San Francisco or London make sure to check out one of their retail locations where you can admire the innovative and stylish design. And if you don’t find yourself in any of these cities, you can check out each unique product line at one of their partner retail locations thanks to the past collaborations.

At the end of the day, amazing brands like MAFIA Bags give us hope that there is still opportunity for a small business to make an impact and grow through a sustainable business model. We thank the innovators at MAFIA Bags for leading the way.

While New York City is overflowing with artists and creatives, one thing the city is always short on is space. This is especially true for musicians who need rehearsal spaces that are both affordable and acoustically sound. That’s where Roberto Romeo (pictured) saw a tremendous opportunity to expand his small business and support the community of local musicians. Read More

An hour before my hotel alarm goes off, I’m thrown awake by a chorus of hammers, trucks and drills from the construction outside. Where am I? Right, Detroit. The city of a legendary decline and an even more legendary revival. I’ve heard enough “dark” stories to shape my groggy and not so pleasant image of this city – but it’s an image that will be shattered in just a few days.

About a month ago, CNote was invited to participate in the FinTech program sponsored by Village Capital and Paypal. The program focuses on supporting entrepreneurs creating innovative financial solutions for underserved communities and small businesses. It is in a perfect alignment with CNote and I was excited for the opportunity to learn from other companies sharing a common mission to democratize finance. Detroit was chosen as a destination for the first program workshop. First skeptical of the choice, once we got there, it became clear why Detroit. On the way from the airport, we passed by urban farms – huge white greenhouses in once deserted parking lots at the borderline of downtown Detroit. Not exactly what I pictured about the city in dismay – I was intrigued.

The next four days we spent together with other 11 companies, learning about the big problems each of us are solving, about huge numbers of underserved individuals and businesses seeking access to basic financial services, and solutions our companies are designing to correct the inequality. To say that it was inspiring is like saying Steve Jobs was just another businessman – each day after hours of intense discussions, hard questions, personal stories about what drives us and why we won’t stop, we left even more energized to work on what could change in the lives of millions.These are people who have been largely ignored by a massive unfeeling financial industry And yes, we are talking about millions…millions who don’t understand what they get charged in their medical costs, millions who can’t drive because they can’t get the car insurance, millions who don’t have emergency funds saved to start their lives after an earthquake, millions whose houses get damaged in the hurricanes, millions who are behind their financial goals, millions who don’t get access to capital to start their business, millions who became a victim of online fraud, millions who can’t pay expenses for the their families in their home countries…These are not just millions, but millions of individuals with their own goals, aspirations, desires, needs which must be respected and met no different from others who are more privileged. And that’s why Village Capital and PayPal brought us together in Detroit to help build the tools that will serve these faceless millions who have been overlooked too long.

As we were getting deeper and deeper into conversations about how broken the existing financial system is, and ways we intend to rebuild it to serve people and to proclaim financial inclusion and financial freedom, I suddenly had an “aha” moment – how symbolic it is to have these discussions in Detroit, the city that was brought down to its knees by human greed, the city that is being brought back to life by human faith, creativity and altruism. It takes a community to rebuild the city, so as the financial system. We could not be in a better company than 11 others in the Village Capital program. We at CNote are excited for what is to come, we hope you are too!

Community Lender Helps Entrepreneur Grow Her Business

La Newyorkina is a place for handmade Mexican ice cream, paletas (ice pops), chamoyadas & other treats. It is also a fan favorite all around New York City. La Newyorkina is known for using unique flavors, fruits, and ingredients in its colorful paletas (Mexican popsicles). The journey to small business success wasn’t always sweet, but this story highlights just how integral a role community lenders can play in helping small businesses succeed, and the positive impact these loans can have on the communities they serve. Read More

We are humbled and proud to share that CNote has been selected to participate in the Village Capital FinTech program. This program, co-sponsored by PayPal and Village Capital, is on a mission to help create “accessible, efficient, and affordable financial services for underserved communities and small businesses.” Such recognition does come with a responsibility to continue what we started – democratizing finance, generating higher returns for everyone, and helping to build and fund underserved communities and entrepreneurs

CNote is one of twelve companies that were selected to participate, each of them “addresses true pain points in the current financial system or intends to expand their services to fill those gaps.” Peer learning and sharing is what makes Village Capital program especially unique and there is certainly a lot to learn from other courageous and inspiring fellow entrepreneurs. To complement, all companies will also receive support and input from member organizations including PayPal, BlackRock, Access Ventures and Village Capital. It truly takes a village to build what people need.

The CNote team is excited about the opportunity this invitation presents and looks forward to spreading the word about our mission to generate higher returns for our customers while making a positive social impact. Stay tuned for the updates about the program progress, our learnings and “a-ha’s”.

You can read more about the Village Capital FinTech program here and here, and read more about CNote and our mission, here.

Did you grow up with a piggy bank? You know, the pink kind that smiles end to end as you proudly plop each copper penny into its thin slat? Plunk. Plink, plink.

Yep, me too.

But, what I’ve come to realize is the psychology behind that little pig is much broader than I thought. To me, that piggy bank was the first representation of “savings” – or the idea of storing money for another day. As a kid, it could sometimes feel like torture, waiting endlessly for that 50 cents to grow to $5 so I could finally buy that special toy. As a teenager, it started to feel like power, where I didn’t have to ask my parents for every purchase. As a grown adult, it feels like safety, knowing that despite the uncertainties of our world today, I’ve got some cash on hand to handles life’s bumps and cool opportunities.

But along that journey, something interesting happened in my mid-twenties. The concept of savings and that piggy bank started to change. It’s when I was informed that dollars in my savings are not just supposed to sit and collect dust – they are actually supposed to work for you while you sleep. Huh?

Then my dad explained to me what actually happens to my savings when it’s in a bank. Despite my fairytale impression that my dollars were sleeping soundly in a big silver vault protected by Vin Diesel, the truth is the complete opposite. My savings dollars – and yours – don’t stay in a big vault at all, but rather get lent out to other people by the bank. This is how the bank “puts the money to work.” It takes my $100 as a “savings deposit” and then loans that $100 to someone else in the form of a home mortgage, credit card or simply buys other investments with it like treasury notes.

What happens next? Oh.. you’ll love this part. The bank then earns money off of our money and returns a portion (and I mean less than 1%) of that earned money back to us – the savers. So when you look at your bank account and see the word “interest” that’s code for:

“Of the money we make off you, here’s how much we’re going to give back to you. Love, Your bank.”

And here’s where the concept of CNote was born. We think, if our money is being used anyway, why not a) give the savers more of those earnings (ie. interest) and b) why not put those dollars to use for good things we care about (ie. supporting local businesses, non-profit, low-income community development, etc).

Sound crazy? Nope.

We think it’s high time we revisited this esoteric concept of “savings” and how the trillions of dollars out there currently don’t go to work for us and our communities, but for the big banks. It’s time to take back our savings and put it to work in ways that drive more earnings for good savers and more goodness for our communities.

CNote is making this happen, every day, by working with inspiring community lenders that are not only certified by the Treasury Department, but have a proven track record of delivering solid financial performance and incredible social impact. It’s how we bring great earnings and impact to everyone.

Tell that childhood piggy bank to stand back. Change is a comin’.

We’re proud to announce that our founders Cat Berman and Yuliya Tarasava have been selected for consideration for the Echoing Green Fellowship. Each year Echoing Green evaluates thousands of applicants and roughly only 1% of applicants are selected. Congratulations are in order for Cat and Yuliya, who are working to democratize and simplify finance through CNote. The two will travel to New York for interviews and could be selected as finalists for the “Echoing Green Fellowships – [a] two year immersive leadership development program that provides seed-funding and hands-on support, and embeds them in the Echoing Green network.”

Echoing Green is a truly remarkable organization that “identifies tomorrow’s transformational leaders today.” Echoing Greenworks to find extraordinary individuals, who have influential ideas and original solutions. “We unite this diverse group of innovators, instigators, pioneers, and rebels to form a fellowship of passionate, global leaders. With access to funding, grants, and strategic foundational support, we can accelerate the positive vision these leaders have for the world.”

These leaders are true change makers dedicated to “transforming their communities, addressing economic development, racial and gender equity, environmental sustainability, and more.”

CNote is honored to be considered for such a high recognition. Our focus on financial freedom and equality is aligned with Echoing Green’s mission, and we look forward to seeing how this opportunity develops.

Who knew the flower business was so competitive? Most of your revenues come from just a few days out of the year and it is a supply chain and logistics nightmare. Not only that, but with online ordering and distribution networks, it takes real dedication and talent to separate yourself from all that competition.

We are beyond excited to announce that CNote was selected as the winner out of a group of five great finalists in the Payment and FinTech Technologies group at SXSW. Every company deserved such a high recognition, but we are thrilled that our that our message resonated with the audience at SXSW and we are the taking “The Top Innovation” award home.

This recognition is an important reminder that there is room to innovate in the financial space, especially as it relates to maximizing individual and societal wealth. CNote makes products that simplify and democratize finance. We focus on inclusivity, integrity and community when creating every financial product we bring to market.

You can learn more about CNote and our mission here. Also, feel free to contact our team with any questions at support@mycnote.com.

CDFIs are a tough acronym to remember. We get it. It stands for Community Development Financial Institutions – yet another mouthful. We think the easiest way to describe them is – lenders for the community.

So..say you have a dream of opening up your own business. You have the drive, a great idea, and all you need is to borrow a few bucks to get it going or keep it going. Unfortunately, your options are not so great.

Sorry to break the news, but not all lenders are the same and the online lenders you’ve heard of typically charge small businesses 6 to 7x more than large banks to access money. Yup.

But wait, this is where CDFIs come in! They provide small businesses fair capital and business coaching. And on top of that, they focus on segments like women and minorities that typically get ignored or rejected by major financial institutions.

So now you’re going: COOL! But why haven’t I heard of them before?

Don’t worry, you haven’t missed the latest fintech trend. The most financially savvy among us haven’t heard of CDFIs.

CDFIs have been around for over 20 years, but have mostly been working with banks and foundations. Their gig wasn’t to approach us – the everyday saver. A few more reasons you haven’t heard of them:

Marketing. CDFIs are awesome at fair and responsible lending. But most of them are non-profits and don’t have the large and expensive marketing budget to get the word out about their good work. Likely the best promotion CDFIs have received was through the Starbucks and Opportunity Finance Network partnership to launch Create Jobs for USA campaign started by Howard Schultz. You may have been one of the hundreds of thousands of individuals who contributed a total of $3.5 million to the successful campaign.

Access. Most CDFIs are set up to take in large dollar amounts from banks and foundations, not small dollar amounts from you and me. So if you called up a CDFI with your $25 check, it would be a tough road to navigate.

Understanding. There are over 1,000 CDFIs across the country. Folks just learning about CDFIs love their social mission, but can find it overwhelming in terms of which CDFI to work with and why. This is a key problem CNote is solving for.

So now you know. CDFIs are awesome, dedicated and doing great work every day. And CNote is excited to bring you and them together to create an incredible economic impact. That means more money and more jobs for women and minorities. It means more investment vehicles that represent your voice and your values. It means finally – finance we can be proud of.

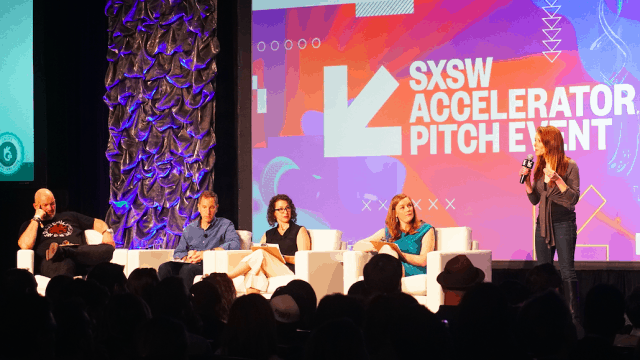

We’re proud to announce that CNote has been selected as a finalist for this year’s South by Southwest Accelerator Pitch event. CNote is one of five payment and FinTech companies selected for the pitch event. We’re excited to share our vision for creating accessible financial products that maximize individual and societal wealth with the “future curious” audience of SXSW.

The pitch event will be held over two days, Saturday, March 11 and Sunday, March 12 at the Hilton Hotel in downtown Austin. If you’re a fan of CNote, or just a fan of seeing innovative companies deliver their message, we recommend checking it out.

All the selected finalists will pitch Saturday and then 18 companies will move on and pitch again one more time on Sunday. You can view the list of all invited companies, including CNote, here.

We’re thrilled to be on the stage with amazing entrepreneurs inspired to change the world and grateful to SXSW for the opportunity to share our mission for redesigning finance. You can learn more about CNote and our mission here. Also, feel free to contact our team at support@mycnote.com with any questions.

A whole new coffee experience

A whole new coffee experience

MAFIA Bags is more than just a series of stylish, functional, and sturdy bags, totes, backpacks and accessories. It is a company which represents community and cohesiveness around two inspirational goals. To give new life to materials and to transform the way we do business.

MAFIA Bags is more than just a series of stylish, functional, and sturdy bags, totes, backpacks and accessories. It is a company which represents community and cohesiveness around two inspirational goals. To give new life to materials and to transform the way we do business.

The next four days we spent together with other 11 companies, learning about the big problems each of us are solving, about huge numbers of underserved individuals and businesses seeking access to basic financial services, and solutions our companies are designing to correct the inequality. To say that it was inspiring is like saying Steve Jobs was just another businessman – each day after hours of intense discussions, hard questions, personal stories about what drives us and why we won’t stop, we left even more energized to work on what could change in the lives of millions.These are people who have been largely ignored by a massive unfeeling financial industry And yes, we are talking about millions…millions who don’t understand what they get charged in their medical costs, millions who can’t drive because they can’t get the car insurance, millions who don’t have emergency funds saved to start their lives after an earthquake, millions whose houses get damaged in the hurricanes, millions who are behind their financial goals, millions who don’t get access to capital to start their business, millions who became a victim of online fraud, millions who can’t pay expenses for the their families in their home countries…These are not just millions, but millions of individuals with their own goals, aspirations, desires, needs which must be respected and met no different from others who are more privileged. And that’s why Village Capital and PayPal brought us together in Detroit to help build the tools that will serve these faceless millions who have been overlooked too long.

The next four days we spent together with other 11 companies, learning about the big problems each of us are solving, about huge numbers of underserved individuals and businesses seeking access to basic financial services, and solutions our companies are designing to correct the inequality. To say that it was inspiring is like saying Steve Jobs was just another businessman – each day after hours of intense discussions, hard questions, personal stories about what drives us and why we won’t stop, we left even more energized to work on what could change in the lives of millions.These are people who have been largely ignored by a massive unfeeling financial industry And yes, we are talking about millions…millions who don’t understand what they get charged in their medical costs, millions who can’t drive because they can’t get the car insurance, millions who don’t have emergency funds saved to start their lives after an earthquake, millions whose houses get damaged in the hurricanes, millions who are behind their financial goals, millions who don’t get access to capital to start their business, millions who became a victim of online fraud, millions who can’t pay expenses for the their families in their home countries…These are not just millions, but millions of individuals with their own goals, aspirations, desires, needs which must be respected and met no different from others who are more privileged. And that’s why Village Capital and PayPal brought us together in Detroit to help build the tools that will serve these faceless millions who have been overlooked too long.

We are humbled and proud to share that CNote has been selected to participate in the

We are humbled and proud to share that CNote has been selected to participate in the

We’re proud to announce that our founders

We’re proud to announce that our founders

We are beyond excited to announce that

We are beyond excited to announce that